By Vanessa Mangru-Kumar // SWNS

NEWS COPY W/ VIDEO + INFOGRAPHIC

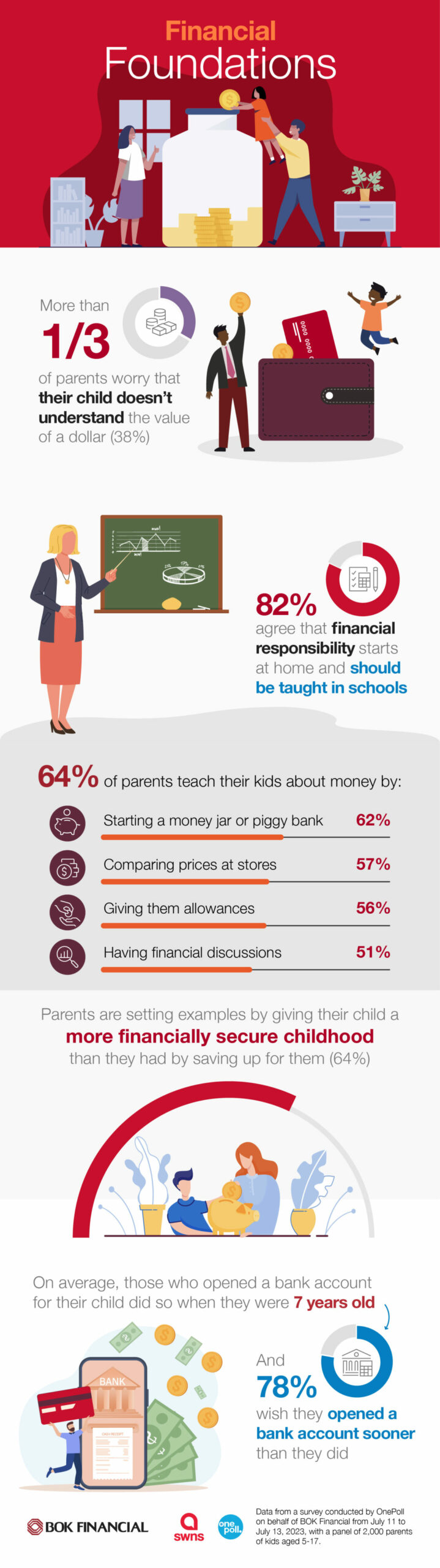

More than a third of parents worry that their child does not understand the value of a dollar (38%), according to new research.

A survey of 2,000 parents of kids aged 5-17 looked at how important they consider financial education early on and found that a majority agree that financial responsibility starts at home (82%).

On average, respondents believe money habits begin to form at 15 years old.

Thus, 85% agree that parents should teach their children the value of a dollar — and how to manage it — before they’re teenagers, or their ability to manage money will suffer in adulthood.

Similarly, 82% agree that children should be taught financial literacy and money management skills in schools.

But the survey, conducted by OnePoll for BOK Financial, found that nearly a third of parents said their child doesn’t learn enough about money in school (29%).

Parents have taken matters into their own hands (64%), teaching kids about saving by starting a money jar or piggy bank (62%) and giving them allowances to help with budgeting (56%).

Other parents teach their children to shop smartly by comparing prices at different stores (57%) or have important financial discussions with them (51%).

The survey also found that the average parent believes someone should have a good understanding of financial literacy by the age of 22.

"If we're not intentional about the financial lessons we're teaching our kids, we're leaving things to chance," said Leasa Melton, consumer product strategy manager at BOK Financial. "Given the importance of financial fitness in a person's long-term wellbeing, parents can be incredibly influential. Even learning simple budgeting skills helps our kids with how to think, solve problems and develop discipline.”

Another 84% said having a job in high school is important for teaching teens about financial responsibility.

Half of those surveyed (51%) said their kids actually do earn money, by selling things like crafts, lemonade or baked goods (63%) or by getting a weekly allowance (57%).

Interestingly, 42% of these parents said their child is monetizing social media accounts to earn money.

Parents also agree that it’s important to set a good example since most believe children are likely to have the same money habits as their parents in adulthood (82%).

One way that parents are setting an example is by making sure their child has a more financially secure childhood than they did by saving up for them (64%).

The average respondent claims they have just under $14,000 in savings for their child.

While most parents surveyed have a bank account for their child (56%), 28% don’t — and may regret it later.

More than three-quarters of those who do have a bank account for their child said that in hindsight, they wish they had set one up sooner (79%).

“While there's no hard and fast rule about opening a bank account or teaching your child about money, the earlier, the better,” said Melton. "We can introduce spending, saving and budgeting to kids at a very young age. Opening a bank account and teaching appropriate money management skills allows your children to ask questions about money and practice their skills in a low-risk environment. These steps help build a solid financial foundation."

METHODS USED BY PARENTS WHO ARE TEACHING KIDS ABOUT MONEY/FINANCES

- Savings jar / piggy bank — 62%

- Shopping and comparing prices — 57%

- Allowances and budgeting — 56%

- Teaching the difference between needs and wants — 56%

- Banking and savings account — 55%

Survey methodology:

This random double-opt-in survey of 2,000 parents of school-aged children was commissioned by BOK Financial between July 11 and July 13, 2023. It was conducted by market research company OnePoll, whose team members are members of the Market Research Society and have corporate membership to the American Association for Public Opinion Research (AAPOR) and the European Society for Opinion and Marketing Research (ESOMAR).